Table of Content

For direct expenses, enter only the amount of expenses allowable for that specific business. These will carry directly to the form and be allowed in full. The IRS doesn't always make it simple to figure out what are personal vs. business expenses when it comes to taxes.

Some examples include the cost of a business telephone line and the cost of painting your home office. However, no deduction is allowed for basic local telephone charges on the first line in your home, even if that line is used for the home office. The same concept relating to direct and indirect expenses applies here. For example, if you buy copy paper for the business or have to repair your home office space. Indirect expenses are once again reimbursed based on a business use percentage. These tasks might include billing customers, keeping books and records, ordering supplies, setting up appointments, or writing reports.

Qualifying for the Home Office Deduction

It's going to be very difficult for Tim to convince the IRS that he is eligible to deduct home office expenses. The Structured Query Language comprises several different data types that allow it to store different types of information... Additional costs incurred that are not related to the use of the home office. It must be a separate structure and disjointed from the main house and only used for business operations. Now multiply the percentage of your home that’s used for business purposes by the amount of the expense. No other part of your home benefits from these expenditures.

Prices for goods and services in Frankfurt are partly crowdsourced by our visitors, just like yourself. Because this area is complex, you should consult a tax professional. Also, you might want to read IRS Publication 587, Business Use of Your Home. One of our CPA's will give you 30 minutes of their time FREE.

Here’s what taxpayers need to know about the home office deduction

Most often, employees working from home bear zero capital gains tax implications for their homes. A home office expense refers to the costs incurred through the performance of business activities within a primary residence. Examples of office expenses may include the internet bill, phone lines, utilities, cost of stationery, taxes, etc. Unless you’re careful, deductions today can cost you money when you sell your home.

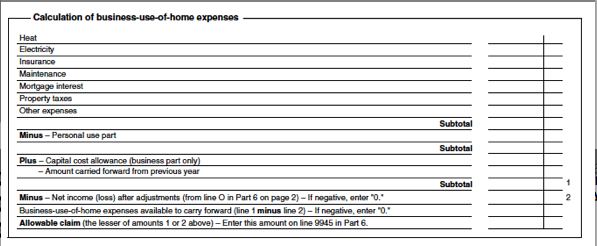

This form starts with the square footage of your dedicated home office space. It compares that to your total home square footage to determine the percentage of your home used exclusively and regularly for business or to store inventory. And your home office uses 10% of the total square feet of your, you would allocate 10% of the indirect expenses to your home office deduction. You can multiply the cost of electricity, gas, trash removal, and cleaning services by your percentage of business use. Your telephone wouldn’t be included because the first telephone line to your house is considered to be for personal use.

Method for Calculating Home Office Expenses

If you maintain a home office and spend money to repair or maintain your house, you need to divide the related expenses between personal and business. Only the expenses that relate to the business portion of your home – your home office – can be included on your Form 8829. If you telecommute or are an employee who works at home, you may also qualify for the home office deduction.

What if your home office is in a separate structure next to your home, like a shed or garage? In that case, it needn’t be your principal place of business. However, you must use that office regularly and exclusively in connection with your trade or business.

As with real estate property taxes, be sure not to deduct your mortgage interest twice if you itemize. Mortgage insurance premiums may also be deducted depending on your income. Some indirect expenses are pretty common and are subject to this equation, along with some other factors that can affect the amount you can deduct. Starting in 2013, the IRS offers a Simplified Method for deducting your home office--if your home office is 300 square feet or less. If your home office is more than 300 square feet you must deduct your home office using the Regular Method. You do not have to use the simplified method, but it's pretty slick.

Be sure you use this structure only for business purposes — you can’t store your car there. An Accountability Plan is the method S Corp owners should employ to take a deduction of their home office expenses. Under this structure, the owner would submit a reimbursement request to the business, and the business would reimburse the owner.

The simplified method significantly reduces your record keeping burden, and saves you time come tax season. The simplified option has a rate of $5 a square foot for business use of the home. Deductions from the business use of a home cannot be claimed if these costs are higher than the home office expenses. Your deduction would be $150 for that $1,000 paint job if you had your entire house painted and your home office takes up 15% of your home’s total square footage. There are three types of expenses you may incur while maintaining a home and home office; direct, indirect, and unrelated.

Be careful not to deduct this one twice if you itemize your deductions on your personal tax return. If you deduct a portion of your property taxes as part of your home office deduction, you must reduce the real estate taxes listed on your Schedule A by that amount. If the gross income from your business equals or exceeds your regular business expenses , all expenses for the business use of your home can be deducted. But if your gross income is less than your total business expenses, certain expense deductions for the business use of your home are limited. As you might expect, this test requires you to show that you exclusively use a portion of your home for business purposes on a regular basis.

Even then, the deductible amount of these types of expenses may be limited. The same space in a home is used exclusively and regularly for conducting business. An allowable area must be established, especially if space changed or was never used in an entire year. According to the IRS, two approaches are used to calculate the number of deductions and how much space constitutes a home office. One of such methods is the regular method, which involves calculating expenses. The second method is the simplified method, which is relatively ineffective since it may not yield a wide range of deductions.

You can deduct both your direct and indirect expenses regarding your home office. Direct expenses are costs that apply only to your home office. You can deduct these costs in full against your business income.

No comments:

Post a Comment